[SatNews] Does the application sell the connectivity, or does the connectivity enable an application (and does it matter whose application)?

In the coming years, a key challenge for maritime service providers will be to turn the “volume markets” (by number of vessels) of merchant shipping or commercial fishing into valuable market segments on a per-vessel basis. Scale obviously rules in these segments now in terms of revenue generation, with more boats equaling more revenues—but, are the tides turning and how quickly can we expect to see the seas change?

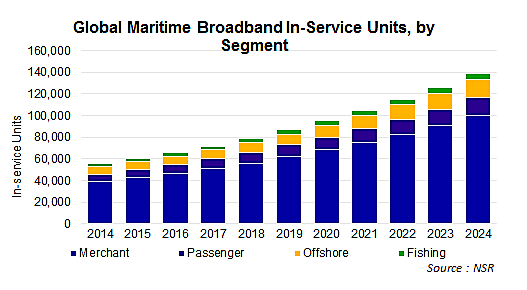

According to NSR’s Maritime Satcom Markets, 3rd Edition 7 out of 10 broadband terminals (both MSS and VSAT) will be in merchant shipping. The segment will be one of the largest sources of retail revenues for service providers, but with a large number of service providers competing in the space for a large number of vessels, the real measure of success will be to steadily increase the amount of value per vessel.

Some steps are easy—Electronic Charting (ECDSIS) is largely a mandate across the merchant fleet, and we’ve already seen a number of offerings aimed at solving that problem. Others, like crew welfare, are a bit more nebulous in terms of what and how those problems can be monetized. Others still, like remote monitoring of onboard equipment, have clear pay-offs, but execution presents even more complications between end-user, service provider, and equipment manufacturer.

All of these really boil down to if service providers need to develop a ‘walled garden’ approach to developing and deploying value-added applications. By that, should service providers develop their own ecosystem of value-added services that are built and optimized for their own networks and equipment, or become an application developer who also happens to provide end-user connectivity? With service providers continuing to purchase value-added providers, it would seem that the market is leaning towards owning the network and the application. But as these applications mature, and the cost of bandwidth decreases with the introduction of HTS, are we going to see a Netflix-Verizon “Pay for Access”-style problem develop within the maritime satcom market as service providers try to encourage adoption of their own value-added offerings?

While a long way off, all the pieces are in place for such a system to quickly develop as we saw in the terrestrial consumer broadband market. Service Providers own the last-mile customer, and end-users are looking to bring more data to/from the vessel to solve their problems (and don’t necessarily want to develop the solutions themselves.) And, each year we continue to see more and more applications enter the market aimed at solving problems within the merchant maritime market. In short, as the entire maritime SATCOM industry is quickly moving from the ‘Internet café’ to ‘BYOD’, how is the industry going to respond to “BYOA” – Bring your own App?

Bottom Line

Will the maritime industry really see similar deals as JetBlue/Exede and Amazon Prime in the aero world? Perhaps, as KVH and Inmarsat recently announced a deal to distribute KVH’s Videotel offering to Inmarsat customers over Inmarsat’s network. And, one can imagine there are similar deals in the works that will turn service providers into ‘application developers.’ The real question still remains to be answered—Does the application sell the connectivity, or does the connectivity enable an application (and does it matter whose application)?