[SatNews] So what happens when companies merge and then merge again?

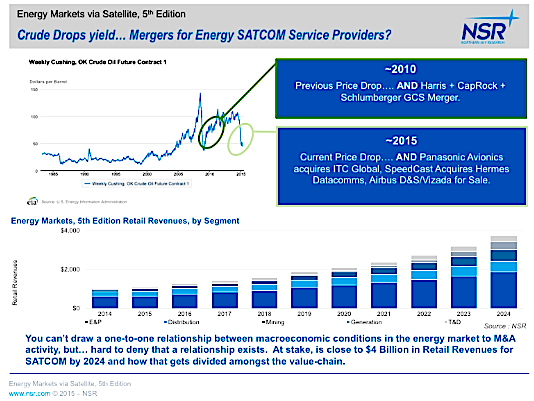

Not since the 2010 merger of Harris-CapRock-Schlumberger GCS has there been change amongst the larger Energy market service providers. However, over the past two weeks Panasonic Avionics Corp. acquired ITC Global, and SpeedCast acquired Hermes Datacomms and Geolink Satellite Services. Meanwhile, Airbus Defense & Space’s commercial SATCOM service division (Vizada), which has a strong presence in the Offshore Support Vessel market, remains for sale. Although it is hard to put a one-to-one relationship between energy market commodity prices (such as crude oil or iron ore), it’s hard to deny that there isn’t at least a casual relationship between them.

As NSR noted in 2011 when the Harris-CapRock-Schlumerger GCS M&A occurred, the impending introduction of HTS capacity into the mobility markets is at-part a consideration of ‘buying end-users’ to increase returns on capacity investments. With the Airbus D&S/Vizada sale still on the market, service providers are taking the first steps in expanding market share and diversifying the vertical markets they serve. For Panasonic, they get the benefit of levering geographic, frequency, and growth rate diversity between the core satellite mobility markets—Aeronautical and Maritime/Energy to further improve their economics of scale to their extensive HTS footprint. For SpeedCast, Hermes is yet another company in a steady string of acquisitions over the past months to increase their presence in the energy sector—and, further increase their presence outside of Asia-Pacific. With aims at becoming a ‘Top 3 player in the energy services space’ there is still probably some additional organic and inorganic growth in the SpeedCast playbook.

Looking forward, not only is the M&A activity likely to continue until the market reaches a new equilibrium around crude oil prices, but now is the time for service providers to encourage end-users to look at new technologies to improve operations.

Just as NSR found in its Energy Markets via Satellite, 5th Edition—the timing of crude oil price collapse couldn’t be better timed for the satellite sector. As a traditionally conservative market, energy market end-users were more likely to embrace the ‘if it aint broke, only change it a little’ approach to acquiring satellite capacity – add a few (or a few dozen depending on the specific sub-segment) Mbps over existing systems and maybe migrate from FSS C-band to FSS Ku-band but, largely wait until HTS options fully mature before jumping on the bandwidth wagon. Now, O&G end-users are looking towards improving operational efficiencies (both in terms of better ‘return’ on their spending, and expanding automation and/or data-centric processes to their remote operations.) All said, new offerings leveraging HTS from GEO, MEO, and in the future LEO, are likely to meet lower resistance from the boardroom

With NSR projecting $4 Billion in Retail Revenues from FSS, HTS and MSS Satellite Communication services by 2024 from the Energy Sector (O&G, Mining, and Electrical Utilities), this changing mindset will help be a key growth driver over the next ten years. For service providers and the value-chain in general, it also opens the door for ‘non-traditional’ or lower-tier players to compete with the bigger brand names. Although track record and legacy will be big hurdles to overcome, the bar has likely dropped a bit as end-users question ‘what they’ve always done.’

Bottom Line

Although disruption to energy market commodity prices is not a necessary condition for greater M&A activity in the SATCOM markets… it is definitely sufficient. Furthermore, as the market settles into a new equilibrium, expect the door into the CIO’s office to be open a bit wider to new technologies, and new players than it might have otherwise. However, the core metrics of success still remain – right service, right location, right price.