[Satnews] At the end of October, the World Radiocommunications Conference 2015 (WRC-15) will commence in Geneva. The most contentious topic of debate being whether to take away rights that satellite operators currently, and for decades, have had for C-band spectrum. Recent years have seen a lot of headlines for HTS, and to a lesser degree Ku-band systems, and the new demand that these satellites can create. However, lost among these headlines is the very real, very diverse, and very much essential market for C-band capacity.

The Market Today

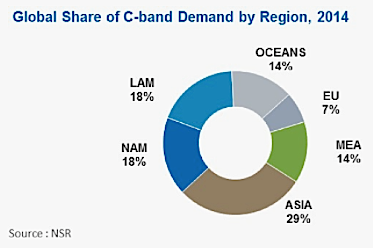

Taking data from NSR’s Global Satellite Capacity Supply & Demand, 12th Edition study, one can identify several key verticals whereby C-band is not only preferred, but oftentimes the only option, or dramatically more efficient than alternatives. This is particularly the case in regions with significant rain fade issues, such as Southeast Asia, and regions with large geographies, such as Ocean regions. As the graph below shows, 2014 saw demand for C-band capacity spread fairly globally, with some of the leading regions including Asia, North America, and Latin America.

C-band For Video Distribution

Different regions utilize C-band capacity in vastly different ways, with wide hemi-type beams being applicable to several different applications. For instance, over 11 percent of Global C-band capacity demand in 2014—or over two hundred 36MHz transponder equivalents (TPEs)—was utilized for Video Distribution in Latin America alone, with Pan-American Spanish language FTA content being far more effective via C-band due to beam size. Other regions that benefit from Video Distribution being broadcast via C-band include significantly more lucrative regions, with North American cable operators and FTA providers leasing nearly 300 TPEs of C-band capacity for video distribution in 2014, equivalent to nearly 1/3 of the global C-band Video Distribution total. All told, nearly 1,000 TPEs of C-band were leased globally for Video Distribution in 2014.

In regions such as North America, proposed exclusion zones for spectrum rights would ultimately end up being very difficult to manage from a Distribution perspective, particularly with more efficient video compression technologies (MPEG-4, for example) leading to small bit errors or frame losses having a stronger adverse impact on video quality.

The USO Play

Further, a number of developing regions, specifically Southeast Asia, South Asia, Sub-Saharan Africa, and Latin America, utilize C-band for Universal Service Obligation (USO) applications, which would largely be backhaul in rural areas. While HTS systems have begun to encroach on these markets, C-band today remains a cost-effective way of delivering low bandwidth backhaul solutions to underserved communities in much of the developing world. With the cost of a full terrestrial backhaul network in rural areas far exceeding the cost of C-band satellite capacity, it remains likely that should terrestrial telcos gain access to C-band spectrum, the economies of scale would not add up to allow for a continued closing of the digital divide, with the only areas likely to have lucrative enough markets to justify the CAPEX being urban areas. Enterprise Data in general remains one of the largest markets for C-band capacity, with over 600 TPEs leased in 2014. And while we know that wide beam Ku band and HTS are proven and less costly alternatives for backhaul, there are still many cases when mobile network operators (MNOs) or sister telcos favor C-band either because of “inertia" or the high availability service levels that regulators demand.

Important to note is many MNOs tend to favor C-band because of its high availability virtues, even in areas that are not too sensitive to rain fade. Here is an interesting paradox because MNOs are pushing for terrestrial access to C-band while they also need it for satellite backhaul in the developing world.

The Market Tomorrow

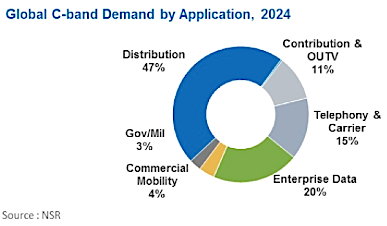

Despite concerns to the contrary, C-band usage is not falling off a cliff anytime soon. NSR does forecast annual declines in C-band capacity usage, with overall demand falling by around 2 percent per year to 2024, however, by this time there will still be around 1,900 TPEs of leased C-band capacity globally, representing over $2.5B in leasing revenues, thousands of TV stations, and orders of magnitude more VSATs, backhaul sites, ships, and more.

Some applications will in fact see solid C-band growth moving forward, with Commercial Mobility, for instance, seeing growth of nearly 4 percent annually. This comes from mission-critical applications onboard vessels in extreme or remote environments, for which C-band is a robust option. Moving forward, applications such as this will continue to provide a solid user base for C-band capacity usage, and while areas of huge growth will come elsewhere, C-band remains a workhorse in terms of specific applications that, when totaled up, represent significant cogs in global trade, development, and media transmission.

Bottom Line

As with any significant policy decision, many factors must be taken into account when the WRC convenes later this month in Geneva. While C-band lacks the flashy headlines of HTS or even Ku-band, it remains a large market currently, with nearly 2,400 TPEs leased globally in 2014. NSR expects it to be utilized in a number of different ways moving forward, with incremental declines in demand not taking away from the fact that there are quite simply a large number of applications for which only C-band capacity is suitable. Given these trends, NSR is strongly against removing C-band spectrum (even lower bands) from the satellite industry and hopes the WRC acts to protect this vital resource that is so important to users worldwide.