[SatNews] In every segment of the telecom industry, lower costs and decreasing prices led to higher market penetration, greater service uptake, and stickiness with end-users and key verticals. The satellite industry has benefited from lower bandwidth pricing, especially across apps like wireless backhaul; however, these prices come with new challenges as well in terms of the ROI picture. While users enjoy lower bandwidth pricing and perhaps more for less, some vendors may struggle with proving ROI as bandwidth prices plummet.

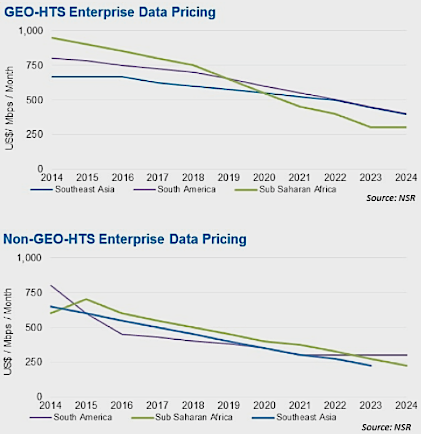

HTS pricing for enterprise data has fallen in the 3 key regions where wireless backhaul usage is expected to exhibit the largest demand. In comparing 2014 and 2015, Non-GEO-HTS (i.e. MEO) prices in particular have fallen at high levels and are expected to continue specifically in South America where a large amount of capacity is to be deployed.

Lower satellite bandwidth costs are positive in general, given that the industry is likely to enlarge its market niche due to a pronounced increase of capacity usage. In the wireless backhaul segment at least, lower bandwidth costs can and will enable 3G, 4G and even 5G services that is in line with the explosive growth of data and video streaming requirements on smartphones, tablets, laptops and over time, perhaps even wearables.

In its latest report, Wireless Backhaul via Satellite, 9th Edition, NSR generated ROI models to support 2G, 3G and 4G services on various satellite platforms. GEO FSS solutions on traditional C-band and Ku-band capacity could generally only support 2G services and a small number of 3G sites. On the HTS front, various solutions could support 3G and 4G services and as the number of sites increased, the ROI became higher and thus sustainable.

One of the key components of profitability and justification from the mobile service operator’s (MSO) perspective will be the lower cost of satellite bandwidth being provisioned by the satellite operator. With a higher number of sites, the MSO will be able to generate higher profits, which should lead to an even higher number of installations over time.

However, the flipside is that lower bandwidth costs will likely create problems on the operator and VSAT vendor side as ROI periods will take longer to be realized. Cheaper bandwidth means longer time for vendors to see net positive ROI for VSAT equipment and capacity, which increases the risks of highly ambitious next-generation programs. Moreover, the investor community, which is an integral piece in enabling competitive and technologically advanced systems, may hold back on funding such programs due once again to a longer payback period.

To illustrate this issue with capacity, if a GEO-HTS program costs roughly US$625 million such as the ViaSat-2 satellite, which includes its launch, insurance and ground infrastructure, pricing capacity at $800 per Mbps per month in order to breakeven on year 1 would need a backlog or sales of 65.1 Gbps of capacity. If priced at $500 per Mbps per month, capacity sales need to increase to 104.2 Gbps to breakeven.

Fortunately for ViaSat, its business model is not solely contingent on capacity sales or the wholesale play. Rather, it is more involved in the retail part of the value chain. Although it can likely sell 60 to 100 Gbps of capacity of its total 160 Gbps total throughput to breakeven via selling capacity for 4G LTE mobile wireless services, ViaSat’s main application is broadband access on its Exede platform. Exede likewise sells to enterprise, aero, government and other verticals where ARPU rates are much higher.

Bottom Line

Is the eventual impact of HTS a good or bad thing? In NSR’s view, it is a very good thing because satellite usage increases and its niche is enlarged due to lower capacity prices to be offered in the marketplace. However, the key is to move up the value chain and not just be a capacity or wholesale player where margins are thin. Rather, a similar model like ViaSat’s Exede, which generates much higher revenues compared to a commodity play, is a better example and better use of HTS capacity in terms of both increasing market penetration and generating revenues.

NSR no longer reports fill rates on HTS satellites simply because the metric is irrelevant. Revenue generation is THE key metric as it can measure ROI and the period where breakeven is accomplished and when profits are realized. As such, a retail play achieves quicker ROI compared to a wholesale or commodity play. Using low cost HTS capacity to internally increase margins via an end-to-end service offering is the way of striking that delicate balance of achieving market penetration and achieving positive revenue generation, and the all-important ROI.