NSR's report regarding the energy markets provides some optimism for an industry that had slowed down, but will be improving.

NSR’s Energy Markets via Satellite, 7th Edition report forecasts the major energy markets to yield nearly $1.6 Billion in Retail Revenues by 2027, up from $900M today. Requiring 80 transponders of FSS capacity and 3.5 Gbps of HTS capacity spread across nearly 280,000 FSS, HTS, and MSS In-Service units for the global Energy Markets, the outlook for Energy SATCOM connectivity is slowly improving. Although revenue growth remains in the low single-digits over much of the forecast period, by 2027 Oil & Gas (the largest opportunity by nearly any metric) remains nearly double the size of both the Mining and Utility segments. Bottom Line, market instability is largely behind the Energy Markets, with a slow return to growth expected over the next ten years.

“It is hard to underestimate the impact the past 12 months have had within the Energy Markets,” states Brad Grady, NSR Senior Analyst and report lead Author. “End-user asset oversupply in the O&G sector, commodity pricing instability for Mining and its impact on natural gas pricing for Utility generation, and political instability in core production markets have all seriously disrupted the status quo. In turn, O&G companies, Mining Players, and Electrical Utilities have all re-analyzed how they do business — putting pricing pressures on suppliers and introducing more technology-centric workflows into remote operations. Satellite Service Providers have been at the forefront of this dynamic change, helping customers introduce HTS in both GEO and Non-GEO to provide throughput and cost advantages, while leveraging capacity pricing changes to keep site of their own financials,” states Grady. The key finding, for major energy markets, is these changes have brought more capacity online without a 1:1 increase in capacity costs.

Offshore Oil & Gas will bear the brunt of these changing dynamics, since end-user expectations are more throughput, with minimal pricing increases. Mining markets continue to be a challenging play; however, the ongoing pricing decline of satellite capacity and digitization efforts across all segments of the lifecycle will propel the Mining market to double service revenue growth over the next ten years. Utilities will more than double their demand for satellite services, with double-digit growth rates expected from 2017 to 2027 as “smart grid” and “utility-scale” generation continue to grow.

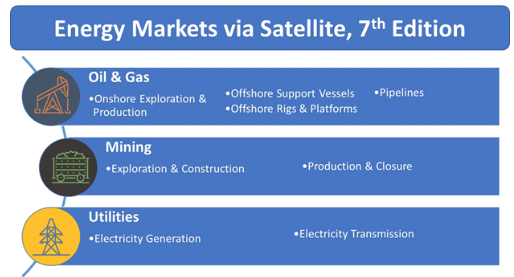

NSR's Energy Markets via Satellite, 7th Edition expands on previous coverage of the Energy Markets. Adding a “by Vessel” view of the Offshore O&G sector, a deeper split of the Mining markets into Exploration & Construction, and Production & Closure, and a revised outlook on the pipeline addressable markets, the report continues NSR’s industry-leading coverage of the energy sector. Focusing on In-service Units, Revenues, and Capacity Demand across FSS, GEO-HTS, Non-GEO HTS, and MSS capacity the report dives-deep into the trends, drivers, and restraints behind each segment.