[Satnews] Ever since NSR coined the phrase “High Throughput Satellite” more than 5 years ago, the industry continues to view HTS as the “next big thing” for satellite telecom. HTS can, if correctly leveraged, be the magic concoction that allows satellite to benefit from the “coverage everywhere” of old, combined with the economies of scale more emblematic of terrestrial communications.

Since the beginning of November, there have been three separate interviews with three industry players outlining the ways in which they intend to alter the industry utilizing HTS, with Greg Wyler of OneWeb speaking with Paris Match (link in French), Mark Dankberg of ViaSat speaking with Space News, and Tom Choi of Asia Broadcast Satellite speaking with Via Satellite. For sure three very different companies with three very different business models, but an undeniable trend emerges in the three discussions—building much bigger HTS payloads than ever before. There has been talk of pricing coming down by 75 percent or more upon the launch of so called “Ultra High Throughput Satellites”, which would obviously have a dramatic impact on the finances of the satellite industry. In a phrase, it would do more than any past advancement to turn satellite into a “dumb pipe” and commoditize capacity to where it can be marketed as strictly bandwidth.

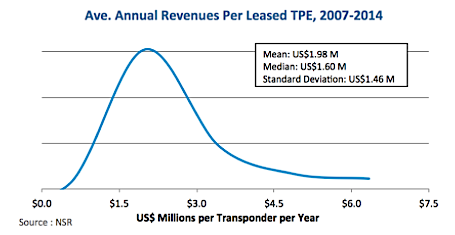

The Impact of LEOs, and HTS Today—Revenues per Leased Transponder

NSR’s Satellite Operator Financial Analysis, 5th Edition delves into these issues at an operator and industry level, with findings indicating a number of trends that bear repeating. The report finds that revenues per leased transponder fell by over 5 percent on average in 2014, with this trend a continuation of the past several years. Interestingly, the industry has thus far not seen major contraction as it relates to top-line revenues, indicating a “pie expansion” in line with decreasing revenues per transponder. Beyond this, standard deviation in this metric has decreased by around $40k per transponder as compared to 2013, indicating that it is becoming more difficult for “brand name” operators to charge premium pricing for their capacity. As the chart below shows, standard deviation remains significant due to several outliers in key markets, but on the whole, pricing converges at a point under $2M per leased transponder, with further declines expected moving forward.

As this trend continues, it will become more essential than ever for operators to either sell a compelling end-to-end “solution”, or to bring down the cost of raw bandwidth to where it can be competitive with terrestrial, at least when taking into account other factors such as reliability and setup costs. As this occurs, margins are likely to fall since there needs to be significantly more capacity leased.

The common anecdote is that when ViaSat-1 was launched, it had as much capacity as all other North American GEO satellites in orbit combined. As such, on a per-satellite basis, margins will fall as more throughput is utilized per satellite despite CAPEX not increasing at a proportional rate. More effort must be put into pushing capacity out the door, particularly as HTS payloads become the only sensible product to put into orbit. Put another way, if an operator were, for example, to put 3 traditional FSS satellites into orbit at a CAPEX of around $1B, vs. 1 “ViaSat-2” type satellite at a CAPEX of $650M, the obvious choice from a raw capacity standpoint is the latter. Given the evolution of the industry towards “more bits for less money”, the second option is virtually the only viable one, and thus moving forward, HTS will be not only a better business case, but in most instances the only business case.

The Impact of LEO-HTS Constellations Tomorrow—Revenues per Mbps and a Pricing Apocalypse?

With LEO-HTS constellations still years away from launch and operation, financial information remains scarce and profitability metrics nonexistent. However, NSR estimates pricing for LEO-HTS broadband could dip as low as $50-60 per Mbps per month following launch, and drop further still once the business model establishes itself. To put this into context, this is around 40% lower than even the lowest-cost GEO-HTS broadband costs, and orders of magnitude lower than leasing prices paid for “connectivity-like” capacity for applications like Enterprise Data and Commercial Mobility, which could theoretically “make the switch” to LEO-HTS should connectivity become the common denominator.

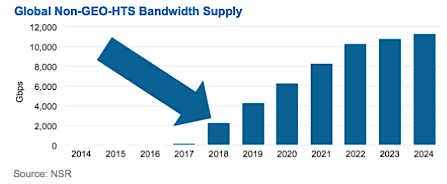

For comparative reference, the chart below from NSR’s Global Satellite Capacity Supply & Demand, 12th Edition shows forecasted Non-GEO-HTS supply coming online to 2024. The 2018 figure, indicated by the arrow, is just over 2 Tbps, or 5 times the amount of GEO-HTS capacity in orbit worldwide at the time of writing.

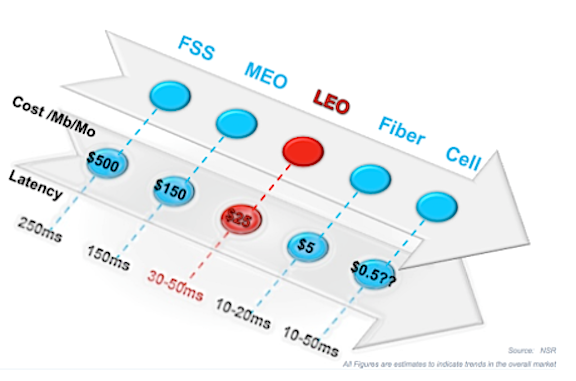

This will significantly bring down the cost of capacity, and force operators to turn their business models on their heads. We have already seen in recent weeks and months a trend towards vertical integration by satellite operators, forging long-term partnerships with, or acquiring outright, service providers or other players in the value chain. This is a trend no doubt brought on by concerns about future competitiveness and being boxed out of the very markets that operators have helped to develop, through building out infrastructure, pushing boundaries of capacity constraints, and helping foster new technologies such as UltraHD. The graphic below, taken from an NSR webinar earlier in 2015, shows the potential development of Mbps cost per delivery method, with LEO-HTS being potentially cheaper than FSS by a factor of 20x on a Mbps basis.

Bottom Line—What Does this All Mean to the Industry Today & Tomorrow?

With Internet connectivity driving all markets and applications, one of the few ways that satellite operators will be able to remain competitive is to increase the “size of the pipe” as it relates to being able to transmit content. Lower pricing is here to stay, and it is likely to accelerate in the coming years, and as content delivery players like satellite telcos or terrestrials continue to see a smaller piece of their legacy pie, the impetus will be on these very companies to find ways to ensure they’re in a better position to capture the rapidly expanding pie of demand for connectivity.

Last week, Cisco announced that global cloud traffic is expected to increase to 8.6 zettabytes by 2019, with 1 zettabyte equal to 1,000 terabytes. Clearly, demand for connectivity is here to stay, and with words like zettabyte being thrown around, it is arguable that players such as OneWeb announcing 10 Gbps satellites at a cost of $400K each, or ViaSat announcing 1 Tbps payloads are not so much revolutionary, as they are evolutionary. There will remain ample opportunities for satellite operators to sell compelling end-to-end solutions, and enormous demand for raw bandwidth at the right price, but the days of $2,000 per Mbps per month for a stationary enterprise VSAT appear to be long gone indeed.